Wednesday, November 10, 2010

options

could possibly sell a put to prepare for a downside signal, and collect theta from the short straddle until the call and put expire...

Tuesday, November 9, 2010

stopped outt

ok stopped out cable and euryen for a loss, still short usdcad, and took a nzdusd long @ 7799.

Currently thinking:

december .80 call is .0173 on cme.

my SL on kiwi is .7699.

if i was to sell the call, my max loss is Spot loss (1000$) + Premium on short call so ~1730. thats ~730 profit if stopped out.

my max profit is options premium - spot price + strike price or .0173 - .7799 +.8000 = .0374 pips...or 3740$

problem being, what todo with a naked short call option until it expires?

Idea for excel sheet is programming a Spot price, option price calculator to try and price out different ways to use this ($ based not pip based). if that makes sense...i am kind of tired.

anyways...NEWS!

Signed up for Calculus as well as Linear Algebra for January at my old University. Online school just wasn't for me.

ALSO:

http://blogs.wsj.com/marketbeat/2010/11/09/chinese-credit-rater-downgrades-us/

dun dun dunnnnnn

Currently thinking:

december .80 call is .0173 on cme.

my SL on kiwi is .7699.

if i was to sell the call, my max loss is Spot loss (1000$) + Premium on short call so ~1730. thats ~730 profit if stopped out.

my max profit is options premium - spot price + strike price or .0173 - .7799 +.8000 = .0374 pips...or 3740$

problem being, what todo with a naked short call option until it expires?

Idea for excel sheet is programming a Spot price, option price calculator to try and price out different ways to use this ($ based not pip based). if that makes sense...i am kind of tired.

anyways...NEWS!

Signed up for Calculus as well as Linear Algebra for January at my old University. Online school just wasn't for me.

ALSO:

http://blogs.wsj.com/marketbeat/2010/11/09/chinese-credit-rater-downgrades-us/

dun dun dunnnnnn

Sunday, November 7, 2010

Thursday, November 4, 2010

Updates

Ok so got stopped out usdchf +3...lol

usdcad was like +115 or something like that.

Current positions:

100k long gbpusd @ 1.6124 current price 1.6263 +/- +139 stop 1.5975 -149

100k long eurjpy @ 114.91 current price 114.89 +/- -3 stop 113.60 -131

100k short usdcad@ 1.0036 current price 1.0030 +/- +6 stop 1.0175 -139

Current Total +/- +142 if stopped total -419

usdcad was like +115 or something like that.

Current positions:

100k long gbpusd @ 1.6124 current price 1.6263 +/- +139 stop 1.5975 -149

100k long eurjpy @ 114.91 current price 114.89 +/- -3 stop 113.60 -131

100k short usdcad@ 1.0036 current price 1.0030 +/- +6 stop 1.0175 -139

Current Total +/- +142 if stopped total -419

Tuesday, October 26, 2010

Forex never sleeps, neither does the fund manager

I have been short USDCAD since early september (1.0474) and still holding a runner + ~2200$.

Went long usdchf last night @ 9713 on daily. ahead of signal but I am profitable + ~1500$.

I have been posting a lot lately, guess I am kind of mulling things over. It's been just over 5 years I think since I started trading and I haven't been live in over a year (actually I think it was 2008). I think demo has made me somewhat reckless, leaving me with the hope that my positions become profitable (even though Id be up a significant amount this year if it wasn't for position sizing on my cable short beginning of the year, and my usdjpy conviction as of late). Been attempting to do this University of London/LSE external study work, but finding that it is really lacking the explanation of a physical classroom (or is it my absolute hate for micro economics?). I haven't been a great student in the past, but these past 2 years I have gone from a C student to an A student in a subject I haven't been good at since elementary. Decided to go back to the previous university and play by their rules. The trade off of having a good name on my piece of paper vs having a piece of paper I can afford is over. Although that piece of paper will make it easier for me to land a job in the finance world, I want to be a fund manager. Will the name help me raise capital? Probably, but what's the point of the name without the record to back it up? All I need is the basics to get my strategy programmed/backtested, then if plausible I can focus on forming the fund. So I won't be making over 300 000/year managing over 100 mio. Whatever. If I can pull good results from 100 000, then eventually, it will be 1mio, etc.

that was a huge block of rant hahaha, guess its my 230am rant time.

-P.

Went long usdchf last night @ 9713 on daily. ahead of signal but I am profitable + ~1500$.

I have been posting a lot lately, guess I am kind of mulling things over. It's been just over 5 years I think since I started trading and I haven't been live in over a year (actually I think it was 2008). I think demo has made me somewhat reckless, leaving me with the hope that my positions become profitable (even though Id be up a significant amount this year if it wasn't for position sizing on my cable short beginning of the year, and my usdjpy conviction as of late). Been attempting to do this University of London/LSE external study work, but finding that it is really lacking the explanation of a physical classroom (or is it my absolute hate for micro economics?). I haven't been a great student in the past, but these past 2 years I have gone from a C student to an A student in a subject I haven't been good at since elementary. Decided to go back to the previous university and play by their rules. The trade off of having a good name on my piece of paper vs having a piece of paper I can afford is over. Although that piece of paper will make it easier for me to land a job in the finance world, I want to be a fund manager. Will the name help me raise capital? Probably, but what's the point of the name without the record to back it up? All I need is the basics to get my strategy programmed/backtested, then if plausible I can focus on forming the fund. So I won't be making over 300 000/year managing over 100 mio. Whatever. If I can pull good results from 100 000, then eventually, it will be 1mio, etc.

that was a huge block of rant hahaha, guess its my 230am rant time.

-P.

twitter!

oh ya! so I caved and made a twitter account!

now you can get my market sentiment updates in near real time!

@confusdeconmist

now you can get my market sentiment updates in near real time!

@confusdeconmist

Programming todo list

I had surgery on the 14th, so have been on medical leave since then. I am also moving back in with parents in November to save some money (sucks to be not making money and still paying bills), try and find a better paying job. Basically saying I have not purchased Matlab yet (checked out the other option posted in comments but it seems less user friendly), but I am going to start planning how I should program this strategy first.

Logical choice would be to program the moving averages first, then setup rules for the different signals.

**stolen from Oanda's website**

http://fxtrade.oanda.com/learn/forex-indicators/ichimoku-kinko-hyo

The Ichimoku Kinko Hyo chart consists of five lines and a cloud. It accepts three configurable time intervals (x,y,z) as parameters and is calculated as follows:

1. Tenkan-Sen (Conversion Line ) = (Highest High + Lowest Low) / 2, for the past x periods

2. Kijun-Sen (Base Line) = (Highest High + Lowest Low) / 2, for the past y periods

3. Chikou Span (Lagging Span) = Today's closing price plotted y periods behind

4. Senkou Span A = (Tenkan-Sen + Kijun-Sen) / 2, plotted y periods ahead

5. Senkou Span B = (Highest High + Lowest Low) / 2, for the past z periods, plotted y periods ahead

The cloud, known as the Kumo, is the space between Senkou Span A and Senkou Span B.

**end of Oanda info**

Additional Kumo information: Usually, the thicker the kumo cloud, the stronger the support/resistance is. Also, there tends to be key levels called kumo shadows whenever the kumo goes sideways and creates a sideways cloud.

ok so There are essentially three types of signals and they have two directions, bearish or bullish.

For all signals, the tenkan must cross the kijun, and the chikou span must be above the previous price action (or below depending on bull/bear). What changes the strength of the signal is whether or not they cross below, inside, or above the kumo (essentially the support/resistance lines in a moving average form).

I think thats pretty good for now.

-Patrick

Logical choice would be to program the moving averages first, then setup rules for the different signals.

**stolen from Oanda's website**

http://fxtrade.oanda.com/learn/forex-indicators/ichimoku-kinko-hyo

The Ichimoku Kinko Hyo chart consists of five lines and a cloud. It accepts three configurable time intervals (x,y,z) as parameters and is calculated as follows:

1. Tenkan-Sen (Conversion Line ) = (Highest High + Lowest Low) / 2, for the past x periods

2. Kijun-Sen (Base Line) = (Highest High + Lowest Low) / 2, for the past y periods

3. Chikou Span (Lagging Span) = Today's closing price plotted y periods behind

4. Senkou Span A = (Tenkan-Sen + Kijun-Sen) / 2, plotted y periods ahead

5. Senkou Span B = (Highest High + Lowest Low) / 2, for the past z periods, plotted y periods ahead

The cloud, known as the Kumo, is the space between Senkou Span A and Senkou Span B.

**end of Oanda info**

Additional Kumo information: Usually, the thicker the kumo cloud, the stronger the support/resistance is. Also, there tends to be key levels called kumo shadows whenever the kumo goes sideways and creates a sideways cloud.

ok so There are essentially three types of signals and they have two directions, bearish or bullish.

For all signals, the tenkan must cross the kijun, and the chikou span must be above the previous price action (or below depending on bull/bear). What changes the strength of the signal is whether or not they cross below, inside, or above the kumo (essentially the support/resistance lines in a moving average form).

I think thats pretty good for now.

-Patrick

Sunday, October 24, 2010

Matlab testing premise

ok so I have given up on the co-integration idea for now, started working on something temorarily more profitable.

Basically going to program my Ichimoku indicator into matlab. Back testing the 6 signals the indicator produces to test for: A. Legnth of trade in days B. profit of signal in pips.

basis being that I wish to use covered calls to help fix my money management strategy. Basically, as ichimoku has a trailing stop loss built in, calculating the average movement of each signal and its legnth would make me able to create a generalised covered call strategy. Effectively limiting my topside, but virtually destroying my downside.

My worries:

Greeks. I am very bad with them, and the only two I see as being against me would be volatility and delta. Delta can be managed by activly changing the size of the spot trade to match the short option position, but still not sure.

I am sick of my positional stragies being right, but at the wrong time. I figure that this strategy can help with that by recovering the cost of being early or just plain wrong.

currently @ parents so will post more later.

Basically going to program my Ichimoku indicator into matlab. Back testing the 6 signals the indicator produces to test for: A. Legnth of trade in days B. profit of signal in pips.

basis being that I wish to use covered calls to help fix my money management strategy. Basically, as ichimoku has a trailing stop loss built in, calculating the average movement of each signal and its legnth would make me able to create a generalised covered call strategy. Effectively limiting my topside, but virtually destroying my downside.

My worries:

Greeks. I am very bad with them, and the only two I see as being against me would be volatility and delta. Delta can be managed by activly changing the size of the spot trade to match the short option position, but still not sure.

I am sick of my positional stragies being right, but at the wrong time. I figure that this strategy can help with that by recovering the cost of being early or just plain wrong.

currently @ parents so will post more later.

Thursday, October 7, 2010

USDJPY

we hit 82.30 dismorning and I closed the position for a loss.

We have a war between the central banks across the world right now. Rumors that EU and BOE bought multiple billions of yen today, making my long even more useless.

sitting out for a while and hitting the theoretical drawing board before I get back in.

We have a war between the central banks across the world right now. Rumors that EU and BOE bought multiple billions of yen today, making my long even more useless.

sitting out for a while and hitting the theoretical drawing board before I get back in.

Tuesday, October 5, 2010

USDJPY

Added some more at 83.22 and 83.24, average is now 83.74.

holding 20 lots long.

market went to re-test the market lows, hopfully this will remain a bullish sign and we will break that 84.25 level with ease.

holding 20 lots long.

market went to re-test the market lows, hopfully this will remain a bullish sign and we will break that 84.25 level with ease.

Monday, October 4, 2010

USDJPY

I have been buying this pair for a week now.

currently holding 1.2 mio long with 83.949 average, with a bid for 200k more at 93.67 (if filled I am playing $140 per 0.01 movement) and the pair currently has a daily ATR of 80 pips over the last 30 days. So potential VaR for the day is +/- 140*80 or $11 200 usd.

I am convicted that USDJPY will rise going into the end of the year, and will keep buying.

currently holding 1.2 mio long with 83.949 average, with a bid for 200k more at 93.67 (if filled I am playing $140 per 0.01 movement) and the pair currently has a daily ATR of 80 pips over the last 30 days. So potential VaR for the day is +/- 140*80 or $11 200 usd.

I am convicted that USDJPY will rise going into the end of the year, and will keep buying.

Monday, September 20, 2010

School

Started my adventure @ UoL via access route.

Planning out my case study to bring to the Brits to get work visa...one step at a time though.

Finding it very difficult to obtain some of the books needed for my mathematics courses here in Canada, or they are just that much cheaper to buy in UK and ship here. Guess thats a good example of trade isn't it? hahahaha (currently stuck on the chapter 1 specialization and trade section)

-P

Looking to get a new toy soon too...thinking about a Seiko Monster...watches are a terrible addiction...

Planning out my case study to bring to the Brits to get work visa...one step at a time though.

Finding it very difficult to obtain some of the books needed for my mathematics courses here in Canada, or they are just that much cheaper to buy in UK and ship here. Guess thats a good example of trade isn't it? hahahaha (currently stuck on the chapter 1 specialization and trade section)

-P

Looking to get a new toy soon too...thinking about a Seiko Monster...watches are a terrible addiction...

Tuesday, August 31, 2010

updates

So I am buying Matlab...all this work in excel is taking too much time. I can just program the formula's and just get it to scan the data.

Also, as I have been going through Dr. Edward Thorp's 'Beat the Market', I have discovered to be what I think is a covered call mispricing on DF (Dean Foods Co.) on september 2010 12.50 calls.

Bid/ask is 0.10/0.15

This is leaving the effective price to be:

long call: 12.65

short call 12.40.

that means I can sell the right to buy at 12.40 on september 17th. Current price of the stock is 10.22.

that effectively is a 20% profit.

Also, as I have been going through Dr. Edward Thorp's 'Beat the Market', I have discovered to be what I think is a covered call mispricing on DF (Dean Foods Co.) on september 2010 12.50 calls.

Bid/ask is 0.10/0.15

This is leaving the effective price to be:

long call: 12.65

short call 12.40.

that means I can sell the right to buy at 12.40 on september 17th. Current price of the stock is 10.22.

that effectively is a 20% profit.

Monday, August 23, 2010

Probability Senario's

***Keep in mind this is a theoretical idea that I am trying to prove right or wrong***

ok so for the eurgbp stat arb/dynamic hedging idea I created 9 different possible outcomes:

1: Euro up Gbp up

2: Euro up Gbp sideways

3: Euro up Gbp down

4: Euro sideways Gbp up

5: Euro sideways Gbp sideways

6: Euro sideways Gbp down

7: Euro Down Gbp Up

8: Euro down Gbp Sideways

9: Euro Down Gbp Down

Going through 1000 ticks (insanely small sample, but I am doing this by hand) for both eurgbp long and then for eurgbp short. Noticing that you have several numbers in a row. Could be what I was looking for. For example, I have a 6 then a 7. Euro goes from 1.4540 to 1.4537, while cable goes from 1.61106 to 1.61143...so that's 3 pips on euro and 3.7 on cable.

Still haven't the faintest idea how to calculate the buy/sell spread into the equation. Looking for someone to help with this possibly (or refer me to a source I could learn from). Just trying to prove that they have possible profitable situations on a statistical level.

ok so for the eurgbp stat arb/dynamic hedging idea I created 9 different possible outcomes:

1: Euro up Gbp up

2: Euro up Gbp sideways

3: Euro up Gbp down

4: Euro sideways Gbp up

5: Euro sideways Gbp sideways

6: Euro sideways Gbp down

7: Euro Down Gbp Up

8: Euro down Gbp Sideways

9: Euro Down Gbp Down

Going through 1000 ticks (insanely small sample, but I am doing this by hand) for both eurgbp long and then for eurgbp short. Noticing that you have several numbers in a row. Could be what I was looking for. For example, I have a 6 then a 7. Euro goes from 1.4540 to 1.4537, while cable goes from 1.61106 to 1.61143...so that's 3 pips on euro and 3.7 on cable.

Still haven't the faintest idea how to calculate the buy/sell spread into the equation. Looking for someone to help with this possibly (or refer me to a source I could learn from). Just trying to prove that they have possible profitable situations on a statistical level.

Friday, July 23, 2010

Hedging strategy

ok so thought of something while reading hulls derivative book last night.

Basis Risk and optimal hedge ratio.

usually used for futures-spot, but I believe I can re-write the formula to be true for spot on spot movements.

i.e you actively sell euro short to hedge your cable position.

more to come later.

Basis Risk and optimal hedge ratio.

usually used for futures-spot, but I believe I can re-write the formula to be true for spot on spot movements.

i.e you actively sell euro short to hedge your cable position.

more to come later.

Thursday, July 22, 2010

updates

started regulating my trade sizing.

currently long cable 1.5176 at my max position of 30% utilization of leverage (1.8million long).

movements from 1.5335 area to 1.5125 area show a retracement range of 1.5230-1.5250.

Price is sitting at 1.5182.

Daily pivot is 1.5205 on my chart.

this means that if we break that pivot I should plan on taking some profits around 1.5230, leaving a runner, and possibly adding around 1.52 on the retrace...that way if 1.52 breaks, I will have taken profits and could then look for next opportunity.

-P.

currently long cable 1.5176 at my max position of 30% utilization of leverage (1.8million long).

movements from 1.5335 area to 1.5125 area show a retracement range of 1.5230-1.5250.

Price is sitting at 1.5182.

Daily pivot is 1.5205 on my chart.

this means that if we break that pivot I should plan on taking some profits around 1.5230, leaving a runner, and possibly adding around 1.52 on the retrace...that way if 1.52 breaks, I will have taken profits and could then look for next opportunity.

-P.

Wednesday, July 7, 2010

recent events

School Application was sent off.

MASSIVE Heatwave in Ottawa, really regretting moving into an apartment without Air conditioning.

Cut out from my standard 6 pairs to focus on one pair. Back to the basics.

Also working on Integration from some random Calculus book I picked up at Chapters.

tis all for now.

MASSIVE Heatwave in Ottawa, really regretting moving into an apartment without Air conditioning.

Cut out from my standard 6 pairs to focus on one pair. Back to the basics.

Also working on Integration from some random Calculus book I picked up at Chapters.

tis all for now.

Monday, June 7, 2010

Listening

funny that when someone tells you something, you take it with a grain of sand until you understand it.

I have been patient, waiting for trades to develop and have been trying to scale in with great results.

started the week with ~73 000 in alpari currenex demo, currently sitting at ~98 000. high water mark is like 110 000 i believe, so still a lot of work to do.

I have been patient, waiting for trades to develop and have been trying to scale in with great results.

started the week with ~73 000 in alpari currenex demo, currently sitting at ~98 000. high water mark is like 110 000 i believe, so still a lot of work to do.

Sunday, May 9, 2010

update sunday night

euro sits at 1.295, thats +0.035, and cable sits at basically 1.488 (+0.002).

thats +350 and +20.

thats +350 and +20.

Thursday, May 6, 2010

Greek debt crisis

So a bunch of greeks went around and cheated the system, pulling their debts off of their balance sheets using swap derivatives. Trichet is giving them abour 150 billion so they will not default. The greek people are striking. They are caught in a catch 22. If they leave the EU they are fucked, if they stay they are fucked.

Anywho,

Majority of the markets are imploding from this. I see this as a chance to test the reflexivity of the markets. As cds's and most markets collapse, one question comes to my head.

Is this really that bad?

We can look at the US bailout, the Russian default of 1998 that crippled ltcm, and the bullrun of 2009.

Fundamentally I am thinking that this is just one of those moments blown out of preportion, and traders with a straight head can make a killing cutting through the bullshit and make serious money.

As I write this the dow is 10630, down 237.76, down 2.19%, euro is 1.26, down 10% in the past month, usdjpy is 90.18, and cable is 1.49.

Interesting would be testing my theory of the equlibrium between similar based currency pairs.

So let's create a paper portfolio. 1 000 000 dollars.

25% equities, remainder fx.

Long dow 10630 for $106300

Short cable 1.49 for 100 000 cable making 149 000 usd.

Long euro for 149 000 usd, or 118 253.97 euro @ 1.26.

100:1 margin for the fx trades:

So that's 1000 for gbp, 1490 for euro.

And no leverage for equity trades,

So total margin is

108 790 for the portfolio. Will start to update this every day to test it out.

Anywho,

Majority of the markets are imploding from this. I see this as a chance to test the reflexivity of the markets. As cds's and most markets collapse, one question comes to my head.

Is this really that bad?

We can look at the US bailout, the Russian default of 1998 that crippled ltcm, and the bullrun of 2009.

Fundamentally I am thinking that this is just one of those moments blown out of preportion, and traders with a straight head can make a killing cutting through the bullshit and make serious money.

As I write this the dow is 10630, down 237.76, down 2.19%, euro is 1.26, down 10% in the past month, usdjpy is 90.18, and cable is 1.49.

Interesting would be testing my theory of the equlibrium between similar based currency pairs.

So let's create a paper portfolio. 1 000 000 dollars.

25% equities, remainder fx.

Long dow 10630 for $106300

Short cable 1.49 for 100 000 cable making 149 000 usd.

Long euro for 149 000 usd, or 118 253.97 euro @ 1.26.

100:1 margin for the fx trades:

So that's 1000 for gbp, 1490 for euro.

And no leverage for equity trades,

So total margin is

108 790 for the portfolio. Will start to update this every day to test it out.

Tuesday, May 4, 2010

death of the euro

Ok so I have an idea,

if you can profit when company a merges with company b via risk arbitrage, can the same not be done with currencies?

Profiting from the breakup of currencies?

if you can profit when company a merges with company b via risk arbitrage, can the same not be done with currencies?

Profiting from the breakup of currencies?

Sunday, April 11, 2010

Cahones and Traders Gut

ok so have a common problem with my trades, and I need to rectify it (somehow haven't rectified it in the past two years)

I have been giving my trades room to breathe, but find that once I add-on to the original trade, I start to think I am wrong all the time.

Most recently I was long cable avg. 1.529x for 20 lots. I had the original idea based on my technical system, that 1.5230 would be my exit. Not following my system, I got out in the 70s, for a substantial loss. Had I gone to bed, I would have made ~17% on the trade, with the low being 1.5265...

I need to calculate a position sizing strategy.

I have been giving my trades room to breathe, but find that once I add-on to the original trade, I start to think I am wrong all the time.

Most recently I was long cable avg. 1.529x for 20 lots. I had the original idea based on my technical system, that 1.5230 would be my exit. Not following my system, I got out in the 70s, for a substantial loss. Had I gone to bed, I would have made ~17% on the trade, with the low being 1.5265...

I need to calculate a position sizing strategy.

Friday, April 9, 2010

Slowly creating a hypothesis.

In the financial crisis of the 2007-2008, we experienced one of the most disastrous tests of modern economic theory.

During the “sub-prime” crash, a mass scale de-leveraging occurred creating events 26 standard deviations outside the normal. Situations such as these are dubbed “Black Swans”, by author Nassim Taleb in his book “The Black Swan: The impact of the highly improbable”. This event tested equilibrium theory to its limits (this is debatable as the limits are set under money management parameters). Major Hedge Funds were hammered relentlessly as their statistical arbitrage strategies reversed, driving further away from equilibrium instead of towards it. This flight to liquidity was seen several years earlier by a firm named Long Term Capital Management (LTCM).

In 1998, a superstar Quantitative Hedge Fund, LTCM, felt that exact pain, and succumb to it. LTCM had a strategy that involved On the Run, and Off the Run US Treasury Bonds. I should start by saying that liquid assets are usually priced higher than non liquid as they are easier to sell off without a large change in price. LTCM’s strategy was to buy the non-liquid 30 year Treasury bonds, and sell short the liquid On the Run 30 year bonds. This is known as relative value investing (or arbitrage in the modern sense of the word). The theory behind the strategy is that as they are essentially the same instrument, they should have the same value, and should converge on an equilibrium level, which shows profits on being both Long the Off the Run bonds, and Short the On the Run bonds. This turned LTCM into one of the largest funds of its time. That was until the Russian Debt Crisis.

LTCM had spread its strategy into many different markets and added massive amounts of leverage to ramp up its profits. As they assumed equilibrium theory would hold, they could profit. Unfortunately LTCM didn’t calculate human error into their models. When Russian defaulted on its debt, it created a flight to liquidity. The very objects LTCM was short, were being driven to the sky, and the investments they were long, were being demolished to bargain basement deals. They decided to keep buying as equilibrium had to be met at some point, but due to their massive leverage (~40:1) they were bleeding money fast.

Could this be an ideal period for the US to introduce their leverage caps on various markets? Probably, but they decided to wait several years and spend trillions of tax payers money before pointing fingers. LTCM was the first of the great Rocket Science Quant firms to fall.

Karl Popper had a theory. He believed that scientific discoveries are theoretically correct until they are proved wrong. So for the financial markets, you may say “this is the worst event to ever happen to the market”, and that would fuel traders to sell short, pummeling the market until it reaches its exhaustion point. This point is where the panic begins to slow, and the market sentiment begins to shift and they begin to buy again. Could this be applied to quantitative models to prevent future meltdowns?

This is where my theory steps in.

In the Foreign Currency market (FX, FOREX) currencies are priced in fractions of another. I.e. when you are bullish (thinking it will go up) on Cable (British Pound), you buy Cable against another currency that you believe is going to go down against Cable. But when you have two similar base currency crosses such as EUR/USD and GBP/USD then theoretically you should be bearish USD or bullish USD, and as the currency pairs have the same base, they should move in correlation with each other, except with different rates of change. This then has the potential to create a similar, profitable situation. Possibly giving the two a value in terms of each other, then modeling the spreads between them could help prove this theory, but the two already have a cross, EUR/GBP. The problem with the cross is that you are directly selling cable for euro when you are bullish, and vice versa for bearish. That is why I want to try and prove that it is possible for one to model, and profit from this statistical relationship. I view it as a much safer trade than simply buying/selling in the spot market. Yes, you do profit on one position, and lose on the other, but the loss is a hedge which is protecting against the spread widening.

To prove this theory I am trying to create sets of rules that need to be followed in order for this to be possible.

Firstly, defining the relationship between EUR/USD, GBP/USD and EUR/GBP is needed to prove that the no arbitrage theory holds. I will continue to use these pairs, but there are many pairs that work for this style of strategy, and some that probably show much greater profits.

Currency Bid (x) Ask (y)

Euro/Usd (e) 1.50(x1) 1.51(y1)

Gbp/Usd (g) 2.00(x2) 2.01(y2)

EurGbp bid = x3 ask = y3

X3 = x1/y2 y3=y1/x2

X3=(1.50)/(2.01) y3=(1.51)/(2.00)

X3=0.7462 y3=0.7550

Therefore,

x1/y2=x3

y1/x2=y3

Else an arbitrage opportunity arises.

..more to come...want to make sure my numbers are correct, worked all day and cannot think straight.

During the “sub-prime” crash, a mass scale de-leveraging occurred creating events 26 standard deviations outside the normal. Situations such as these are dubbed “Black Swans”, by author Nassim Taleb in his book “The Black Swan: The impact of the highly improbable”. This event tested equilibrium theory to its limits (this is debatable as the limits are set under money management parameters). Major Hedge Funds were hammered relentlessly as their statistical arbitrage strategies reversed, driving further away from equilibrium instead of towards it. This flight to liquidity was seen several years earlier by a firm named Long Term Capital Management (LTCM).

In 1998, a superstar Quantitative Hedge Fund, LTCM, felt that exact pain, and succumb to it. LTCM had a strategy that involved On the Run, and Off the Run US Treasury Bonds. I should start by saying that liquid assets are usually priced higher than non liquid as they are easier to sell off without a large change in price. LTCM’s strategy was to buy the non-liquid 30 year Treasury bonds, and sell short the liquid On the Run 30 year bonds. This is known as relative value investing (or arbitrage in the modern sense of the word). The theory behind the strategy is that as they are essentially the same instrument, they should have the same value, and should converge on an equilibrium level, which shows profits on being both Long the Off the Run bonds, and Short the On the Run bonds. This turned LTCM into one of the largest funds of its time. That was until the Russian Debt Crisis.

LTCM had spread its strategy into many different markets and added massive amounts of leverage to ramp up its profits. As they assumed equilibrium theory would hold, they could profit. Unfortunately LTCM didn’t calculate human error into their models. When Russian defaulted on its debt, it created a flight to liquidity. The very objects LTCM was short, were being driven to the sky, and the investments they were long, were being demolished to bargain basement deals. They decided to keep buying as equilibrium had to be met at some point, but due to their massive leverage (~40:1) they were bleeding money fast.

Could this be an ideal period for the US to introduce their leverage caps on various markets? Probably, but they decided to wait several years and spend trillions of tax payers money before pointing fingers. LTCM was the first of the great Rocket Science Quant firms to fall.

Karl Popper had a theory. He believed that scientific discoveries are theoretically correct until they are proved wrong. So for the financial markets, you may say “this is the worst event to ever happen to the market”, and that would fuel traders to sell short, pummeling the market until it reaches its exhaustion point. This point is where the panic begins to slow, and the market sentiment begins to shift and they begin to buy again. Could this be applied to quantitative models to prevent future meltdowns?

This is where my theory steps in.

In the Foreign Currency market (FX, FOREX) currencies are priced in fractions of another. I.e. when you are bullish (thinking it will go up) on Cable (British Pound), you buy Cable against another currency that you believe is going to go down against Cable. But when you have two similar base currency crosses such as EUR/USD and GBP/USD then theoretically you should be bearish USD or bullish USD, and as the currency pairs have the same base, they should move in correlation with each other, except with different rates of change. This then has the potential to create a similar, profitable situation. Possibly giving the two a value in terms of each other, then modeling the spreads between them could help prove this theory, but the two already have a cross, EUR/GBP. The problem with the cross is that you are directly selling cable for euro when you are bullish, and vice versa for bearish. That is why I want to try and prove that it is possible for one to model, and profit from this statistical relationship. I view it as a much safer trade than simply buying/selling in the spot market. Yes, you do profit on one position, and lose on the other, but the loss is a hedge which is protecting against the spread widening.

To prove this theory I am trying to create sets of rules that need to be followed in order for this to be possible.

Firstly, defining the relationship between EUR/USD, GBP/USD and EUR/GBP is needed to prove that the no arbitrage theory holds. I will continue to use these pairs, but there are many pairs that work for this style of strategy, and some that probably show much greater profits.

Currency Bid (x) Ask (y)

Euro/Usd (e) 1.50(x1) 1.51(y1)

Gbp/Usd (g) 2.00(x2) 2.01(y2)

EurGbp bid = x3 ask = y3

X3 = x1/y2 y3=y1/x2

X3=(1.50)/(2.01) y3=(1.51)/(2.00)

X3=0.7462 y3=0.7550

Therefore,

x1/y2=x3

y1/x2=y3

Else an arbitrage opportunity arises.

..more to come...want to make sure my numbers are correct, worked all day and cannot think straight.

Tuesday, March 30, 2010

Example of strategy using made up numbers

Euro bid/ask: 1.50/1.51

Cable bid/ask: 2.00/2.01

Market moves, Euro increases more than Cable:

Euro Bid/Ask: 1.60/1.61

Cable Bid/Ask: 2.05/2.06

so if euro was over valued in relation to cable, I would go short euro and long cable creating:

Euro: ($100)

Usd: $160

Gbp: $77.66

Usd: ($160)

Momentum hits cable as USD is being sold off, rates become:

Euro bid/ask: 1.63/1.64

Cable bid/ask: 2.20/2.21

So your position becomes:

Euro: ($100)

Usd: $163.00

Gbp: 77.66

Usd: ($171.63)

you would then cover your position creating:

Euro: $100

Usd: ($164.00)

Cable: ($77.66)

Usd: $170.85

Profit in USD including theoretical spreads being: P=170.85-164.00 =$6.85

Now to calculate margin requirement so that you can calculate RoR %:

Leverage: 10:1

Euro Margin (EM) : $16.50

Cable Margin (CM): $16.50

Profit (P) = 6.85

RoR (%) = [P/(EM+CM)]*100

Thus:

RoR = [6.85/33.00]*100

Ror = 20.76%

Now biggest Item would be how to price one in relation to the other so that it is possible to spot these type of positions...

Time to goto the Library!

Cable bid/ask: 2.00/2.01

Market moves, Euro increases more than Cable:

Euro Bid/Ask: 1.60/1.61

Cable Bid/Ask: 2.05/2.06

so if euro was over valued in relation to cable, I would go short euro and long cable creating:

Euro: ($100)

Usd: $160

Gbp: $77.66

Usd: ($160)

Momentum hits cable as USD is being sold off, rates become:

Euro bid/ask: 1.63/1.64

Cable bid/ask: 2.20/2.21

So your position becomes:

Euro: ($100)

Usd: $163.00

Gbp: 77.66

Usd: ($171.63)

you would then cover your position creating:

Euro: $100

Usd: ($164.00)

Cable: ($77.66)

Usd: $170.85

Profit in USD including theoretical spreads being: P=170.85-164.00 =$6.85

Now to calculate margin requirement so that you can calculate RoR %:

Leverage: 10:1

Euro Margin (EM) : $16.50

Cable Margin (CM): $16.50

Profit (P) = 6.85

RoR (%) = [P/(EM+CM)]*100

Thus:

RoR = [6.85/33.00]*100

Ror = 20.76%

Now biggest Item would be how to price one in relation to the other so that it is possible to spot these type of positions...

Time to goto the Library!

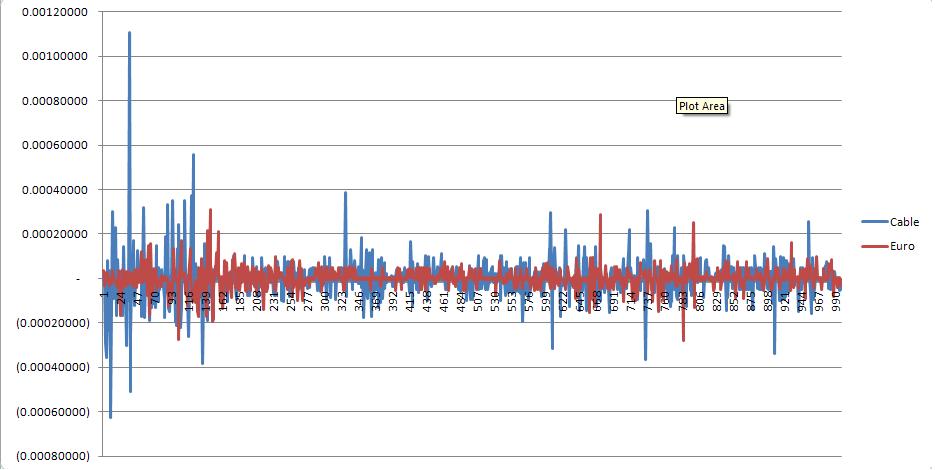

Statistical Arbitrage Idea (Attempt #1)

Ok so I want to try and prove that there is a way to profit (including spread) between two correlated FX pairs.

I picked Euro and Cable over 1000 ticks (thanks to Leslie for finding truefx.com).

Basically I gave a mean value for the bid/ask just to prove if the theory could even work, then created a +/- value for each tick from the median. So Each new tick is either + or - the previous. Notice how there are a couple very large movements on cable, while euro does not move much? I think that this proves that there is potential in my idea.

I think the next step is that I need to find a way to give value to each pair in value of the other, this will give a base to see if its profitable with spreads. Then I need to prove if the prices revert so that the position could be closed.

edit: I know its not much data to prove the point, but figured testing small sample first to create the calculations would be better than dealing with many lines.

Sunday, March 28, 2010

QME

ok so I have my last test on Trig, Exponential Functions, and Logarithmic functions on Wednesday March 31st, and then my exam on April 7th.

Started trying to plan out my undergrad so that I can be well equiped for MFE, or CQF, and started to build a reading list.

Going to pick up Ross' Introduction to Probability Theory this week, and picked up Thorp's 'Beat the Dealer' because I couldn't find a reasonably priced 'Beat the market' (which I found at the University's library :) ).

anywho...lots of over extended markets tonight, took USDJPY short @ 92.6610...might be adding EURYEN and GBPYEN but depends on how it reacts to the highs its going into.

Started trying to plan out my undergrad so that I can be well equiped for MFE, or CQF, and started to build a reading list.

Going to pick up Ross' Introduction to Probability Theory this week, and picked up Thorp's 'Beat the Dealer' because I couldn't find a reasonably priced 'Beat the market' (which I found at the University's library :) ).

anywho...lots of over extended markets tonight, took USDJPY short @ 92.6610...might be adding EURYEN and GBPYEN but depends on how it reacts to the highs its going into.

Monday, March 8, 2010

finally

Spent the last 3 weeks cleaning a virus off of my computer.

Finally have it fixed, and everything back to normal.

Took dllryen short 91.929 before I started fighting the virus, and thankfully forexnews.com allows me to track rates from my blackberry. Currenex is Java based so works from almost anywhere which is helpful for next time.

anywho.

I am still bearish markets, and insanely bullish on inflation right now. Almost to the point that we should be worried.

The economy cannot handle inflation until it sees more jobs.

As for me going to live trading again I have steps setup, I just need things to fall into place.

I need a constant source of income for the summer. If that happens, I go live in September while at school using fractual compounding MM, and logical market analysis. I have been networking my ass off to find something I can get full-time hours, but nobody is hiring yet. I hope to hear back within the next couple weeks or I will intensify even more.

I need to get back to trading, and stop making excuses as to why. If I want something I need to take it, Its not going to jump and land on my lap.

Finally have it fixed, and everything back to normal.

Took dllryen short 91.929 before I started fighting the virus, and thankfully forexnews.com allows me to track rates from my blackberry. Currenex is Java based so works from almost anywhere which is helpful for next time.

anywho.

I am still bearish markets, and insanely bullish on inflation right now. Almost to the point that we should be worried.

The economy cannot handle inflation until it sees more jobs.

As for me going to live trading again I have steps setup, I just need things to fall into place.

I need a constant source of income for the summer. If that happens, I go live in September while at school using fractual compounding MM, and logical market analysis. I have been networking my ass off to find something I can get full-time hours, but nobody is hiring yet. I hope to hear back within the next couple weeks or I will intensify even more.

I need to get back to trading, and stop making excuses as to why. If I want something I need to take it, Its not going to jump and land on my lap.

Sunday, January 31, 2010

Updates...

So starting to become frustrated with my trading.

While I have been going over my Jan010 trades, I have noticed common problems:

A. I have issues with position sizing for the account. I need to learn how to scale into a position. Started with 1:1 and ended up 14:1 on the account, only to have it go the direction I was feeling after I was stopped out (was short cable). This leads me to show that my logic is correct, it is just my timing and Risk Management that needs to be addressed.

B. Time commitment. I cannot afford to sit in front of the computer trading a demo account. Simply as that. Paper Profits cannot pay bills. Even if it is for the track record.

C. Capital. I Cannot deem trading anything under $100k. It doesn't pay the bills, even on good months. Unless there is salary involved (even if its small). Seeing how my trading methodology is based on sustainability, you cannot be sustainable when you cannot pay your bills.

Starting to come to conclusion that trading is becoming a hobby and not a goal. I take two steps forward, and three back. Work is slow, but not slow enough to give me adequate time to trade. Slow means no money, this is leaving me to look for a second job just to pay rent. Becoming worried that if I even get into Quantitative Economics @ university for September, I will not have enough cash to stay there. Becoming a sink or swim mindset...paying my way into a prop firm will put me another $5k into debt (making $10k) but has the possibility to push my foot in the door for a track record (prop firm pays 50% commission). But if I preform poorly, then I am out 5k and I go home to $10k of debts with a terrible job. I honestly do not know what to do anymore other than get a second job and try to keep afloat.

“Strength does not come from winning. Your struggles develop your strengths. When you go through hardships and decide not to surrender, that is strength.”

While I have been going over my Jan010 trades, I have noticed common problems:

A. I have issues with position sizing for the account. I need to learn how to scale into a position. Started with 1:1 and ended up 14:1 on the account, only to have it go the direction I was feeling after I was stopped out (was short cable). This leads me to show that my logic is correct, it is just my timing and Risk Management that needs to be addressed.

B. Time commitment. I cannot afford to sit in front of the computer trading a demo account. Simply as that. Paper Profits cannot pay bills. Even if it is for the track record.

C. Capital. I Cannot deem trading anything under $100k. It doesn't pay the bills, even on good months. Unless there is salary involved (even if its small). Seeing how my trading methodology is based on sustainability, you cannot be sustainable when you cannot pay your bills.

Starting to come to conclusion that trading is becoming a hobby and not a goal. I take two steps forward, and three back. Work is slow, but not slow enough to give me adequate time to trade. Slow means no money, this is leaving me to look for a second job just to pay rent. Becoming worried that if I even get into Quantitative Economics @ university for September, I will not have enough cash to stay there. Becoming a sink or swim mindset...paying my way into a prop firm will put me another $5k into debt (making $10k) but has the possibility to push my foot in the door for a track record (prop firm pays 50% commission). But if I preform poorly, then I am out 5k and I go home to $10k of debts with a terrible job. I honestly do not know what to do anymore other than get a second job and try to keep afloat.

“Strength does not come from winning. Your struggles develop your strengths. When you go through hardships and decide not to surrender, that is strength.”

Subscribe to:

Posts (Atom)