Ok so I want to try and prove that there is a way to profit (including spread) between two correlated FX pairs.

I picked Euro and Cable over 1000 ticks (thanks to Leslie for finding truefx.com).

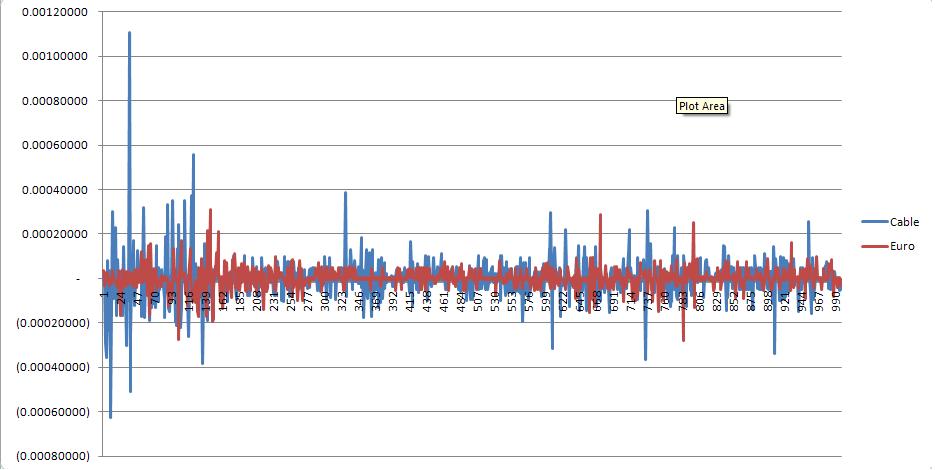

Basically I gave a mean value for the bid/ask just to prove if the theory could even work, then created a +/- value for each tick from the median. So Each new tick is either + or - the previous. Notice how there are a couple very large movements on cable, while euro does not move much? I think that this proves that there is potential in my idea.

I think the next step is that I need to find a way to give value to each pair in value of the other, this will give a base to see if its profitable with spreads. Then I need to prove if the prices revert so that the position could be closed.

edit: I know its not much data to prove the point, but figured testing small sample first to create the calculations would be better than dealing with many lines.

No comments:

Post a Comment