Euro bid/ask: 1.50/1.51

Cable bid/ask: 2.00/2.01

Market moves, Euro increases more than Cable:

Euro Bid/Ask: 1.60/1.61

Cable Bid/Ask: 2.05/2.06

so if euro was over valued in relation to cable, I would go short euro and long cable creating:

Euro: ($100)

Usd: $160

Gbp: $77.66

Usd: ($160)

Momentum hits cable as USD is being sold off, rates become:

Euro bid/ask: 1.63/1.64

Cable bid/ask: 2.20/2.21

So your position becomes:

Euro: ($100)

Usd: $163.00

Gbp: 77.66

Usd: ($171.63)

you would then cover your position creating:

Euro: $100

Usd: ($164.00)

Cable: ($77.66)

Usd: $170.85

Profit in USD including theoretical spreads being: P=170.85-164.00 =$6.85

Now to calculate margin requirement so that you can calculate RoR %:

Leverage: 10:1

Euro Margin (EM) : $16.50

Cable Margin (CM): $16.50

Profit (P) = 6.85

RoR (%) = [P/(EM+CM)]*100

Thus:

RoR = [6.85/33.00]*100

Ror = 20.76%

Now biggest Item would be how to price one in relation to the other so that it is possible to spot these type of positions...

Time to goto the Library!

Tuesday, March 30, 2010

Statistical Arbitrage Idea (Attempt #1)

Ok so I want to try and prove that there is a way to profit (including spread) between two correlated FX pairs.

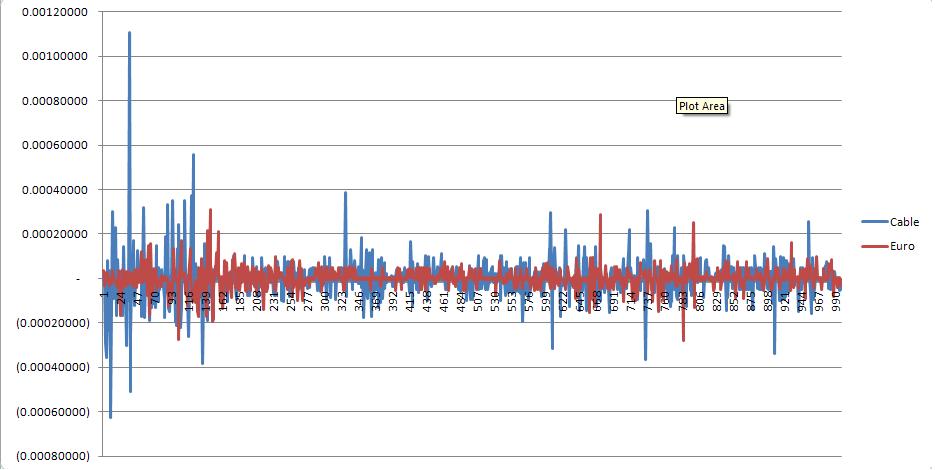

I picked Euro and Cable over 1000 ticks (thanks to Leslie for finding truefx.com).

Basically I gave a mean value for the bid/ask just to prove if the theory could even work, then created a +/- value for each tick from the median. So Each new tick is either + or - the previous. Notice how there are a couple very large movements on cable, while euro does not move much? I think that this proves that there is potential in my idea.

I think the next step is that I need to find a way to give value to each pair in value of the other, this will give a base to see if its profitable with spreads. Then I need to prove if the prices revert so that the position could be closed.

edit: I know its not much data to prove the point, but figured testing small sample first to create the calculations would be better than dealing with many lines.

Sunday, March 28, 2010

QME

ok so I have my last test on Trig, Exponential Functions, and Logarithmic functions on Wednesday March 31st, and then my exam on April 7th.

Started trying to plan out my undergrad so that I can be well equiped for MFE, or CQF, and started to build a reading list.

Going to pick up Ross' Introduction to Probability Theory this week, and picked up Thorp's 'Beat the Dealer' because I couldn't find a reasonably priced 'Beat the market' (which I found at the University's library :) ).

anywho...lots of over extended markets tonight, took USDJPY short @ 92.6610...might be adding EURYEN and GBPYEN but depends on how it reacts to the highs its going into.

Started trying to plan out my undergrad so that I can be well equiped for MFE, or CQF, and started to build a reading list.

Going to pick up Ross' Introduction to Probability Theory this week, and picked up Thorp's 'Beat the Dealer' because I couldn't find a reasonably priced 'Beat the market' (which I found at the University's library :) ).

anywho...lots of over extended markets tonight, took USDJPY short @ 92.6610...might be adding EURYEN and GBPYEN but depends on how it reacts to the highs its going into.

Monday, March 8, 2010

finally

Spent the last 3 weeks cleaning a virus off of my computer.

Finally have it fixed, and everything back to normal.

Took dllryen short 91.929 before I started fighting the virus, and thankfully forexnews.com allows me to track rates from my blackberry. Currenex is Java based so works from almost anywhere which is helpful for next time.

anywho.

I am still bearish markets, and insanely bullish on inflation right now. Almost to the point that we should be worried.

The economy cannot handle inflation until it sees more jobs.

As for me going to live trading again I have steps setup, I just need things to fall into place.

I need a constant source of income for the summer. If that happens, I go live in September while at school using fractual compounding MM, and logical market analysis. I have been networking my ass off to find something I can get full-time hours, but nobody is hiring yet. I hope to hear back within the next couple weeks or I will intensify even more.

I need to get back to trading, and stop making excuses as to why. If I want something I need to take it, Its not going to jump and land on my lap.

Finally have it fixed, and everything back to normal.

Took dllryen short 91.929 before I started fighting the virus, and thankfully forexnews.com allows me to track rates from my blackberry. Currenex is Java based so works from almost anywhere which is helpful for next time.

anywho.

I am still bearish markets, and insanely bullish on inflation right now. Almost to the point that we should be worried.

The economy cannot handle inflation until it sees more jobs.

As for me going to live trading again I have steps setup, I just need things to fall into place.

I need a constant source of income for the summer. If that happens, I go live in September while at school using fractual compounding MM, and logical market analysis. I have been networking my ass off to find something I can get full-time hours, but nobody is hiring yet. I hope to hear back within the next couple weeks or I will intensify even more.

I need to get back to trading, and stop making excuses as to why. If I want something I need to take it, Its not going to jump and land on my lap.

Subscribe to:

Posts (Atom)